The first loan of my life!

With each passing day, the MBA life becomes more and more a reality for Joyjeet. He is someone who cannot help but worry himself to death over everything. After spending the last week worrying about hostel life, he has a new obsession now- choosing the best education loan for MBA in India. One afternoon, he engages his father Mr. Banerjee in a discussion:

Joyjeet: ‘All these years, studying was free! I mean, for me at least…’

Mr. Banerjee: ‘You are right, but I can tell you how much it cost if you feel guilty…’

Joyjeet: ‘Oh come on Dad! Don’t pull my leg…I have enough on my plate with this education loan!’

Mr. Banerjee: ‘Why are you so tense? You know that we can afford the MBA fees but you yourself insist on the loan!’

Joyjeet: ‘I know but this is a great chance for me to take on some financial responsibility. I may still need your support in the future, but for now…’

Mr. Banerjee: ‘I understand, so why don’t you read up about educational loans in India? You can even talk to some of your friends or my friends working in banks. I am sure this is easier than your CAT exam…’

Joyjeet:’Ah, I always do this don’t I! Making a mountain out of a mole…thanks Dad! I shall be bothering everyone who I think can help for the next few days now!’

Mr. Banerjee: ‘You have my blessings…’

Know thy policy

It is natural to be overwhelmed by the sheer number of loan products available in the market. Every scheme can look attractive if you do not know what you are looking for. The best way to clear the clutter is to first realise what you are entitled to by default.

The Indian Banks Association has drafted a model loan scheme for higher education. It has been backed by RBI and serves as a base for banks to structure educational loans. The purpose of the scheme is to make higher education affordable for all students.

In the following sections we will look at the most relevant aspects of the scheme for MBA aspirants.

Which courses qualify for loans as per the scheme?

This should not be a major worrying factor for most students. Top MBA colleges in India such as IIMs, XLRI, JBIMS, FMS and others easily qualify for this. Additionally, the scheme mentions ‘recognised colleges/universities recognised under UGC/Government/AICTE’. This would cover all reputed institutes, whether regional or national.

The key factor that banks look into is the placement potential, which is something that aspirants do as well. Hence, one can be more or less sure of being able to secure an education loan for MBA in India.

What types of expenses are covered under the loan?

The major expenses include basic tuition fee and other mandatory fees such as hostel, library, mess etc. Spending on books, computer, project work etc. is also covered. When calculating the loan amount, the full amount of mandatory expenses (tuition fee etc.) is considered. Other expenses such as expenses for books etc. may only be partially covered.

How much loan can an MBA student avail?

The scheme suggests general ceilings for higher educational loans. A student seeking an education loan for MBA in India can thus avail a loan of up to 10 lakhs. However, this limit is only indicative.

Students getting into top institutes can avail a higher loan amount. Moreover, loans exceeding 10 lakhs can still qualify for the interest subsidy which is usually applicable for loans below 10 lakhs.

Is there a margin requirement?

Margin means a portion of the loan that the borrower has to pay on his/her own. No margin is required for loans up to 4 lakhs. For loans above 4 lakhs, a 5% margin is applicable. There are provisions for securing ‘Nil’ margin loans up to 7.5 lakhs under the Credit Guarantee scheme.

Is there a need for securing the loan?

For an education loan for MBA in India up to 4 lakhs, there is no need for a security. Loans above 4 and up to 7.5 lakhs require a security, which can be in the form of a third party guarantee. Loans above 7.5 lakhs require a collateral security that is suitable to the bank.

Except for special cases, banks require parents to be joint borrowers for any such loan.

What about the interest rate?

Interest rates may vary depending on the size and attributes of the loan. However, simple interest has to be charged till the repayment term begins.

How long will the loan approval take?

The approval for an education loan for MBA in India usually takes about 2-3 weeks. Leadings banks and loan institutes may process loans much faster. If the bank is rejecting the application, the controlling authority of the branch should be involved in the decision. Also, the reason for rejection is to be conveyed to the student.

How long is the repayment holiday period?

The repayment holiday/moratorium is generally the duration of the course plus one year. There are some important suggestions that the scheme makes in this regard:

- Banks can consider giving a relief for periods of unemployment during the loan tenure. Such relief can be given 2-3 times for a period of 6 months each.

- Students who set up their own business venture can be given a moratorium of 2 years.

- A 2 year extension can be granted to students unable to complete the course in the standard tenure.

- If a student services the interest accrued during the course and moratorium before the repayment term begins, he/she is eligible for a 1% subsidy in interest.

- EMI in the initial years can be lower, with a step-wise increase subsequently, such that EMI is proportionate with salary.

What other factors have to be considered?

Insurance

Certain banks may require the student to have life insurance coverage so as to be eligible for the loan.

Processing charges

Banks generally do not charge a processing fee, as per the suggestion of the scheme. However, some banks/third party lenders may charge a fee.

As mentioned earlier, the suggestions of the policy are meant as guidelines. Loan policies can vary greatly from lender to lender.

In short, the key factors to watch out for are…

- Interest rate

- Moratorium/repayment holiday

- Convenience in terms of applying, documenting process

- Flexibility in EMI amounts and scheduling

- Processing fee

- Additional benefits such as interest subsidy, credit guarantee

Why should you consider going for an education loan for MBA in India?

The best student loans in India are a very attractive proposition

Student loans fall under the priority sector lending norms for Indian banks. Consequently, borrowers can avail the benefits of very favourable terms

- Low interest rates

- Simple interest till the moratorium

- Interest subsidies on early repayment

- Relaxed security and margin requirements

Tax savings

Interest repayments on educational loans are tax deductible under section 80E of the Income Tax Act.

A good start for your credit history

Proper repayment of educational loan can boost your credit score. If this is your first loan, it can be a great beginning for your credit record. It can thus help in forming a strong base for seeking loans in the future.

In other words, an education loan for MBA in India is perhaps the most beneficial loan you can avail.

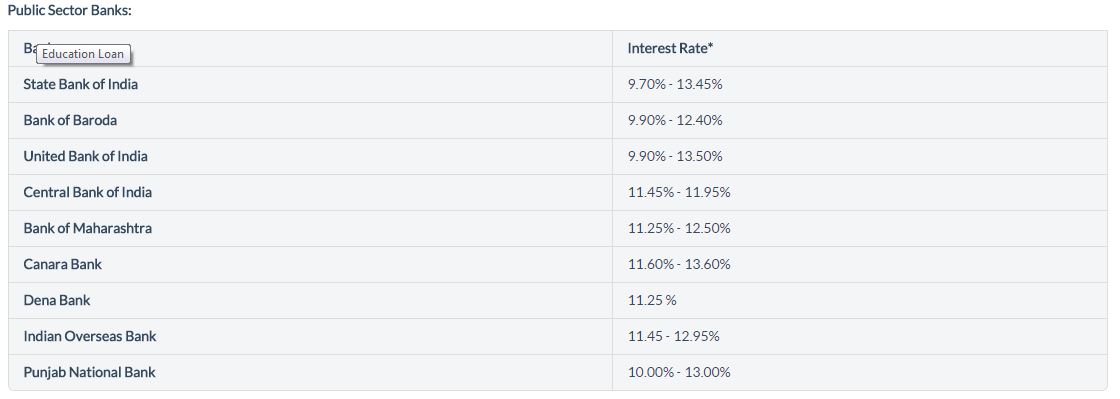

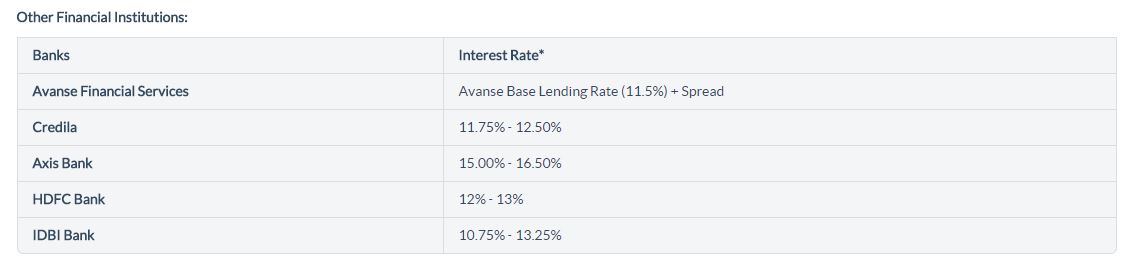

Comparing student loans on offer

There are numerous information portals and blogs which go into the specifics of loan schemes of various banks. For starters, you can see a summary of interest rates offered by some prominent banks and financial institutions below:

Source: Bank Bazaar

Source: Bank Bazaar

Taking a cue from Mr. Banerjee, we recommend reading up all you can on the various loan schemes. You can also consult friends or peers who are likely to be well-informed on this topic.

Or, you can simply shoot a query to our experts here at Praqtise. We will be glad to resolve any student loan related queries. Please share with us in the comments.

—

Image Source